CBDCs and Stablecoins

Section IX: Applications and Synthesis

Army Cyber Institute

April 9, 2026

Agenda

- Types of Digital Money — CBDCs, stablecoins, and traditional cryptocurrencies defined

- Trust Architecture — how control is built into (or out of) each system

- Central Bank Digital Currencies — who is building them and why

- Global Payment Infrastructure — the rails that move money across borders

- Stablecoins — mechanics, major players, and real-world use cases

- Why Governments Care — sovereignty, sanctions, and the permission layer

- Case Study: USDT on Tron — the framework applied

Objectives

By the end of this lesson, you will be able to:

Distinguish CBDCs, stablecoins, and cryptocurrencies by issuer, infrastructure, and state visibility.

Apply the currency layer vs payment infrastructure layer framework to analyze threats to state control.

Assess geopolitical implications: sovereignty, sanctions, capital flows, and infrastructure fragmentation.

Types of Digital Money

| Type | Issuer | Infrastructure | State Visibility | Example |

|---|---|---|---|---|

| Central Bank Digital Currency (CBDC) | Central bank | State-controlled digital ledger | High — programmable, traceable | China e-CNY |

| Stablecoins | Private company or protocol | Public or permissioned blockchain | Varies — USDC (moderate) to DAI (low) | USDT, USDC, DAI |

| Traditional Cryptocurrencies | Protocol (no single issuer) | Permissionless blockchain | Low — pseudonymous | Bitcoin, Ethereum |

The issuer and the infrastructure are separable — that separation is what creates geopolitical tension.

Not all governments pursue all three: China banned private stablecoins (February 2026); the US legislatively blocked a federal CBDC (July 2025).

Central Bank Digital Currencies (CBDCs)

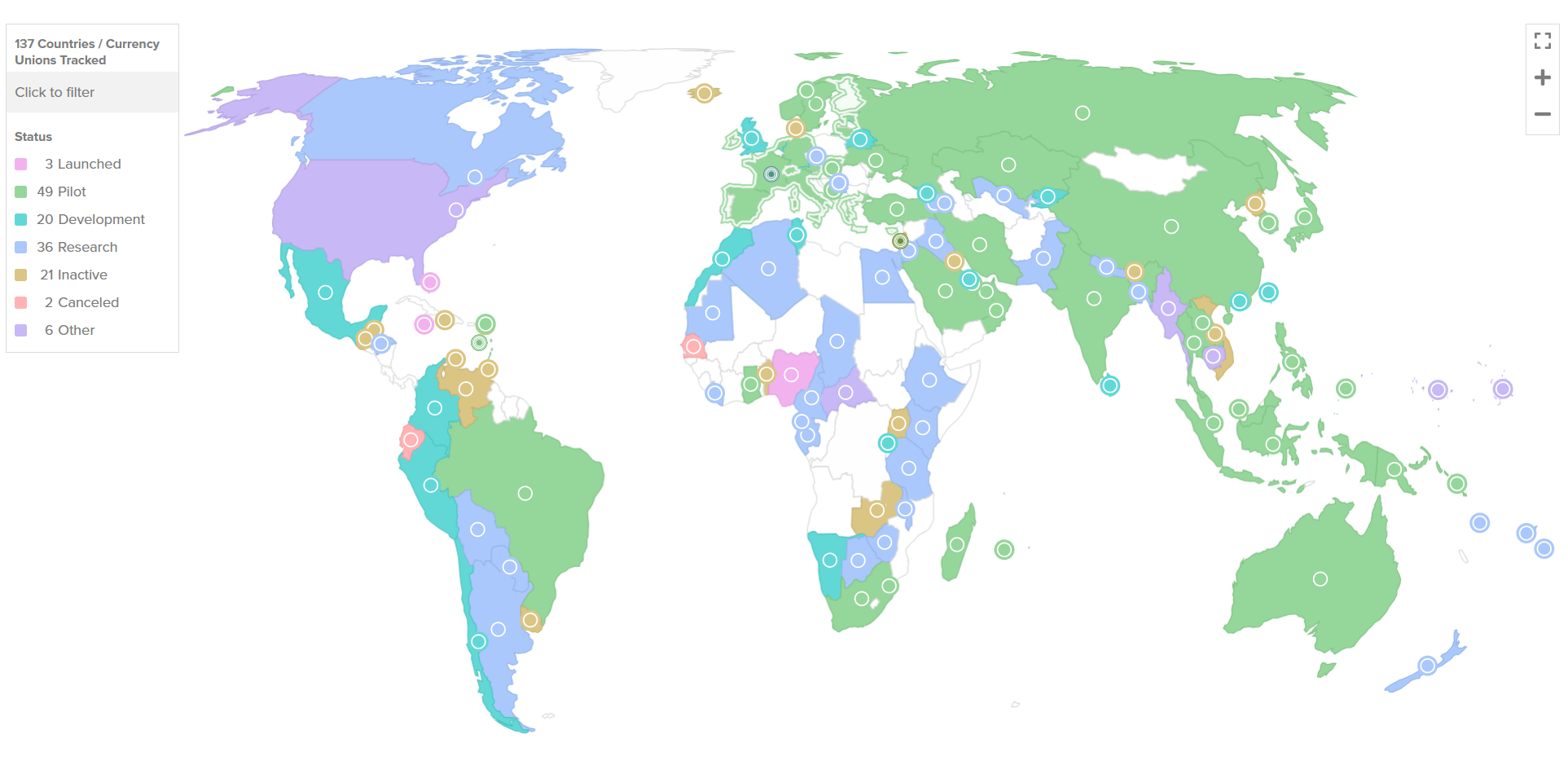

137 countries (98% of global GDP) are exploring a CBDC; 72 are in advanced stages; 49 pilots are active worldwide.

All CBDC designs are permissioned by definition — no sovereign builds on infrastructure it cannot control.

Retail CBDCs: public-facing digital currency for citizens and businesses.

Wholesale CBDCs: interbank settlement systems for financial institutions.

Trust Architecture: CBDCs vs Permissionless Systems

CBDC: Hierarchical Trust (PKI-like)

- Trust flows downward from a root authority

- Every participant is credentialed by a higher authority

- The root can revoke at any level

- No participation without authorization

Permissionless: Distributed Trust (No CA)

- Trust is emergent from consensus, not delegated

- Anyone can generate keys and participate

- No single entity can revoke or freeze

- Security from cryptography + economics, not authority

Global CBDC Landscape

- 3 launched, 49 pilots, 20 in development, 36 researching — the US is an outlier, having legislatively blocked a retail CBDC.

CBDC Technical Platforms

| Platform | Type | Permission Model | CBDC Users |

|---|---|---|---|

| Hyperledger Fabric | Permissioned DLT | Private membership (MSP) | Some pilots, enterprise |

| Hyperledger Besu | Enterprise Ethereum | Permissioned or public | Nigeria (eNaira), Brazil (Drex) |

| Hyperledger Iroha | Permissioned DLT | Role-based access | Cambodia (Bakong) |

| R3 Corda | Distributed ledger | Permissioned | Sweden (e-Krona), Canada (Jasper) |

| Quorum | Ethereum fork | Consortium | Singapore (Ubin), South Africa |

| Tezos | Public blockchain | Permissionless | France wholesale experiments |

| mBridge Ledger | Custom CBDC DLT | Central bank only | China, UAE, Thailand, HK, Saudi Arabia |

| Bitt Platform | Proprietary | Central bank controlled | DCash (ECCU) |

| eCurrency Mint | Centralized | Central bank controlled | Jamaica (JAM-DEX) |

Global Payment Infrastructure: Overview

Money moving across borders travels on rails — messaging and settlement systems that were built long before blockchain existed.

Two functions: messaging (instructions about who pays whom) and settlement (the actual movement of value). These are often separate systems.

The dominant rails are American: SWIFT carries messages; Fedwire and CHIPS settle dollars. Foreign banks reach the dollar system through US correspondent banks — every layer is a potential choke point.

Sanctions power flows from infrastructure control: cutting a country off SWIFT or US correspondent banking is one of the most powerful non-military tools available.

Alternatives are emerging: CIPS (China), SPFS (Russia), and mBridge (CBDC settlement) each reduce dependence on US-controlled infrastructure.

The rise of digital money — stablecoins on permissionless chains, CBDCs on sovereign ledgers — is inseparable from this competition for infrastructure control.

Global Payment Infrastructure: Compare and Contrast

| System | Description | Operator | Function | Reach | US Leverage | Key Limitation |

|---|---|---|---|---|---|---|

| SWIFT | The global “postal service” for bank-to-bank financial messages; does not move money itself | SWIFT (Belgium, US-influenced) | Messaging — carries transfer instructions between banks | 11,000+ institutions, 200+ countries | High — most dollar transactions clear through US correspondents | Messaging only; doesn’t settle. Disconnection is a major sanction tool (Russia 2022) |

| Fedwire / CHIPS | The US domestic systems where dollars actually settle; the foundation of global dollar clearing | Federal Reserve / The Clearing House (US) | Settlement — where dollars actually move | US domestic + international dollar clearing | Maximum — the dollar’s home rails | Only handles USD; foreign banks need US correspondents to access |

| CIPS | China’s cross-border yuan system; combines messaging and settlement, reducing dependence on SWIFT | People’s Bank of China | Messaging + settlement for yuan cross-border transactions | 1,400+ institutions, 110+ countries | Low — operates independently of US infrastructure | Limited to yuan-denominated transactions; still growing reach |

| SPFS | Russia’s SWIFT replacement, built after Crimea sanctions to ensure domestic banks could still communicate | Central Bank of Russia | Messaging — Russia’s SWIFT alternative (est. 2014) | ~550 institutions, mostly Russia + former Soviet states | None — built to avoid US/EU leverage | Very limited international reach; not widely trusted outside allies |

| mBridge | A new model: central banks settle directly in each other’s digital currencies, no correspondent banking needed | Consortium (China, UAE, Thailand, HK, Saudi Arabia) | Direct CBDC-to-CBDC settlement — bypasses correspondent banking | Pilot stage; 5 central banks + observers | None — settles without touching dollar infrastructure | Still experimental; governance and scaling unresolved |

- SWIFT + Fedwire/CHIPS = the current US-centered system. CIPS, SPFS, and mBridge = emerging alternatives. The fragmentation is already underway.

Stablecoins: Types and Mechanisms

Fiat-collateralized: reserves of dollars or equivalents back each token (USDT, USDC).

Crypto-collateralized: on-chain collateral, often over-collateralized (DAI).

Algorithmic: supply adjustments attempt to maintain peg without full collateral.

The collateral model determines redemption risk, transparency, and regulatory surface.

Trust Architecture: The Stablecoin Hybrid

- Issuer layer: centralized, CA-like — can mint, freeze addresses, comply with sanctions (USDC) or not (USDT offshore)

- Network layer: permissionless, no CA — anyone can receive, hold, and transfer tokens without identity verification

- The gap: issuer can freeze known addresses reactively, but cannot gate participation at the network level — users transact peer-to-peer without issuer approval

- This hybrid is why stablecoins are the most contested category — governments have partial leverage (issuer) but not full control (network)

Major Stablecoins and Use Cases

USDT (Tether): largest by volume; dominant on Tron for emerging-market payments.

USDC (Circle): US-regulated; can freeze addresses; sanctions-compliant.

DAI (MakerDAO): decentralized governance; crypto-collateralized; permissionless.

Use cases: DeFi liquidity, international payments, crypto market settlement, inflation hedging.

In practice: shops in Bolivia price goods in USDT; Venezuela’s economy is substantially rewired to stablecoins; Iran’s citizens use Tron-based USDT to hedge a collapsing rial.

CBDCs vs Cryptocurrencies

| Dimension | CBDCs | Cryptocurrencies (Bitcoin, Ethereum) |

|---|---|---|

| Issuer | Central bank (state liability) | No single issuer (protocol rules) |

| Infrastructure | Permissioned — state controls nodes, validation, participation | Permissionless — anyone can run a node, validate, transact |

| Identity | KYC required; state knows participants | Pseudonymous; no identity gate at protocol level |

| Supply control | Central bank sets monetary policy | Fixed or algorithmic supply; no policy discretion |

| Censorship | State can freeze, block, or reverse transactions | Censorship-resistant by design; no single point of control |

| Privacy | Design choice — ranges from cash-like to fully traceable | Pseudonymous on-chain; privacy depends on chain and user behavior |

| Cross-border | Requires bilateral or multilateral agreements (e.g., mBridge) | Borderless by default; no permission needed |

| Legal status | Legal tender in issuing jurisdiction | Varies by jurisdiction — legal, restricted, or banned |

- CBDCs extend state control into digital infrastructure. Cryptocurrencies remove the state from the loop entirely. Stablecoins sit between them — which is why they are the most contested.

Why Governments Care

Monetary sovereignty: control over currency issuance and monetary policy transmission.

Payment system modernization: faster, cheaper, more resilient domestic payments.

Financial inclusion: reaching unbanked populations with digital infrastructure.

Sanctions enforcement and capital flow control: maintaining the state’s ability to restrict and surveil financial activity.

The Permission Layer: Three Challenges to State Control

Bitcoin/Ethereum challenge the currency layer — they propose alternative units of value. A slow, theoretical threat for most major economies.

Stablecoins challenge the payment infrastructure layer — they distribute existing currencies outside sovereign banking channels. An immediate, operational threat.

CBDCs are the state’s attempt to own both layers — the currency and the rails.

Case Study: USDT on Tron

Tron carries a large share of USDT transfers—low fees enable small-value payments.

Functions as de facto dollar infrastructure in economies with capital controls or unstable currencies — Venezuela collects ~80% of oil revenue in USDT; Bolivia shops display USDT price tags.

Local governments lack visibility and control; the US has limited reach over Tron validators.

Demonstrates the gap between issuer control (Tether froze $182M in a single action, Jan 2026) and network control (no one entity controls Tron).

mBridge: A Test Case

- Cross-border payments still rely on correspondent banks, messaging layers, and intermediary checkpoints

- mBridge began in 2021 through the Bank for International Settlements (BIS) Innovation Hub, with China, Hong Kong, Thailand, and the UAE; Saudi Arabia later joined as a full participant

- mBridge asks: can central banks settle more directly on a shared digital platform using their own currencies?

mBridge So Far

- In 2021, the prototype showed that transfers and foreign exchange (FX) transactions could settle in seconds, run 24/7, and lower costs

- In 2022, the pilot handled real value: 20 banks completed 164 transactions worth more than $22 million

- In 2024, BIS said mBridge had reached minimum viable product (MVP) stage: usable for broader testing, but not yet a mature global production system

- Cross-border rule alignment remains a friction point: Countries still have to agree on compliance, data visibility, dispute handling, and network membership

References

[1]

Atlantic Council, “Central Bank Digital Currency Tracker.” Accessed: Oct. 20, 2025. [Online]. Available: https://www.atlanticcouncil.org/cbdctracker/

[2]

D. Boneh and V. Shoup, “Policy and Cryptocurrencies (CBDCs).” 2020. Available: https://intensecrypto.org/public/lec_24_policy.html

[3]

M. Labonte and P. Tierno, “Key Issues in Stablecoin Legislation in the 119th Congress,” Congressional Research Service, Washington, D.C., In Focus IF12984, Sep. 2025. Accessed: Sep. 12, 2025. [Online]. Available: https://www.congress.gov/crs_external_products/IF/PDF/IF12984/IF12984.3.pdf

[4]

BIS, “Annual Economic Report 2022,” Bank for International Settlements (BIS), Annual AR2022E, Jun. 2022. Available: https://www.bis.org/publ/arpdf/ar2022e.pdf

[5]

D. Yaga, P. Mell, N. Roby, and K. Scarfone, “Blockchain technology overview,” National Institute of Standards and Technology, Gaithersburg, MD, NIST IR 8202, Oct. 2018. doi: 10.6028/NIST.IR.8202.

[6]

S. Nakamoto, “Bitcoin: A Peer-to-Peer Electronic Cash System.” Satoshi Nakamoto Institute, Oct. 31, 2008. Accessed: Sep. 12, 2025. [Online]. Available: https://cdn.nakamotoinstitute.org/docs/bitcoin.pdf

[7]

Bank for International Settlements, “Project mBridge reaches minimum viable product stage.” Accessed: Mar. 18, 2026. [Online]. Available: https://www.bis.org/press/p240605.htm

[8]

Hyperledger, “A Blockchain Platform for the Enterprise — Hyperledger Fabric Docs main documentation.” Accessed: Oct. 27, 2025. [Online]. Available: https://hyperledger-fabric.readthedocs.io/en/release-2.5/

[9]

Swift, “Get started with Swift.” Accessed: Mar. 18, 2026. [Online]. Available: https://www.swift.com/your-needs/banking/get-started-with-swift

[10]

World Bank, “Financial sector.” Accessed: Mar. 18, 2026. [Online]. Available: https://www.worldbank.org/en/topic/financialsector

[11]

Bank for International Settlements Innovation Hub Hong Kong Centre, Hong Kong Monetary Authority, Bank of Thailand, Digital Currency Institute of the People’s Bank of China, and Central Bank of the United Arab Emirates, “Project mBridge: Connecting economies through CBDC,” Bank for International Settlements, Oct. 2022. Accessed: Mar. 25, 2026. [Online]. Available: https://www.bis.org/publ/othp59.htm

[12]

MIT Digital Currency Initiative, “Stablecoin Redemptions: For Some, Not All.” 2022. Available: https://www.dci.mit.edu/dci-news/stablecoin-redemptions-for-some-not-all

[13]

U.S. CFTC, “CFTC Orders Tether to Pay $41 Million.” 2021. Available: https://www.cftc.gov/PressRoom/PressReleases/8450-21

[14]

Reuters, “TerraUSD collapse.” Accessed: Mar. 23, 2026. [Online]. Available: https://www.euronews.com/next/2022/05/11/fintech-crypto-currency-terra

[15]

Tether, “How It Works.” 2025. Available: https://tether.to/en/how-it-works

[16]

Circle, “Introducing USD coin.” Accessed: Mar. 23, 2026. [Online]. Available: https://www.circle.com/blog/introducing-usd-coin

[17]

International Monetary Fund, “IMF fintech notes.” Accessed: Mar. 18, 2026. [Online]. Available: https://www.imf.org/en/Publications/fintech-notes

[18]

CoinDesk, [Online]. Available: https://www.coindesk.com/policy/2025/03/06/tether-freezes-usd28m-usdt-on-russian-crypto-exchange-garantex

[19]

Bank for International Settlements Innovation Hub Hong Kong Centre, Hong Kong Monetary Authority, Bank of Thailand, Digital Currency Institute of the People’s Bank of China, and Central Bank of the United Arab Emirates, “Inthanon-LionRock to mBridge: Building a multi CBDC platform for international payments,” Bank for International Settlements, Sep. 2021. Accessed: Mar. 25, 2026. [Online]. Available: https://www.bis.org/publ/othp40.htm

[20]

B. Quarmby, “Tether’s role in Venezuela, Iran highlights the duality of stablecoins,” Cointelegraph. Accessed: Mar. 17, 2026. [Online]. Available: https://cointelegraph.com/news/tether-role-venezuela-iran-highlights-stablecoin-duality

[21]

A. Wood, “Fiat inflation drives crypto adoption across the globe,” Cointelegraph. Accessed: Mar. 17, 2026. [Online]. Available: https://cointelegraph.com/news/fiat-inflation-crypto-adoption-globe

[22]

A. Wood, “Stablecoin A7A5 grows parallel system for sanctioned companies,” Cointelegraph. Accessed: Mar. 17, 2026. [Online]. Available: https://cointelegraph.com/news/stablecoin-a7a5-parallel-network-sanctioned-companies

[23]

D. Staff, “China formalizes ban on yuan stablecoins, RWA tokenization,” Decrypt. Accessed: Mar. 17, 2026. [Online]. Available: https://decrypt.co/357221/china-formalizes-ban-on-yuan-stablecoins-rwa-tokenization

[24]

Dzilla, “U.S. House embeds anti-CBDC provision into NDAA: Implications for crypto innovation and financial privacy,” Dzilla. Accessed: Mar. 17, 2026. [Online]. Available: https://dzilla.com/u-s-house-embeds-anti-cbdc-provision-into-ndaa-implications-for-crypto-innovation-and-financial-privacy/

[25]

C. Comben, “Ray Dalio’s world order warning revives case for Bitcoin as neutral money,” Cointelegraph. Accessed: Mar. 17, 2026. [Online]. Available: https://cointelegraph.com/news/dalio-collapse-world-order-permissionless-money

[26]

D. Staff, “Iran accepting crypto payments for weapons—but this may not help it evade sanctions,” Decrypt. Accessed: Mar. 17, 2026. [Online]. Available: https://decrypt.co/353868/iran-accepting-crypto-payments-for-weapons-but-this-may-not-help-it-evade-sanctions

[27]

A. Haqshanas, “Senators ask Bessent to probe $500M UAE stake in Trump-linked WLFI,” Cointelegraph. Accessed: Mar. 17, 2026. [Online]. Available: https://cointelegraph.com/news/senators-urge-cfius-probe-uae-stake-trump-linked-wlfi

[28]

G. Matos, “Senator Lummis says US military generals support strategic Bitcoin reserve,” CryptoSlate. Accessed: Mar. 17, 2026. [Online]. Available: https://cryptoslate.com/senator-lummis-says-us-military-generals-support-strategic-bitcoin-reserve/

CBDCs and Stablecoins — Army Cyber Institute — April 9, 2026